Retention Modeling & Operations

> Engineering a machine learning pipeline to mitigate revenue loss through proactive retention strategy.

Target Recall

74%

Churn Detection Rate

Baseline Churn

20%

Historical Revenue Leak

Model Champion

Gradient Boost

Optimized with SMOTE

Key Driver

Age & Depth

Primary Churn Signals

Analysis Visuals

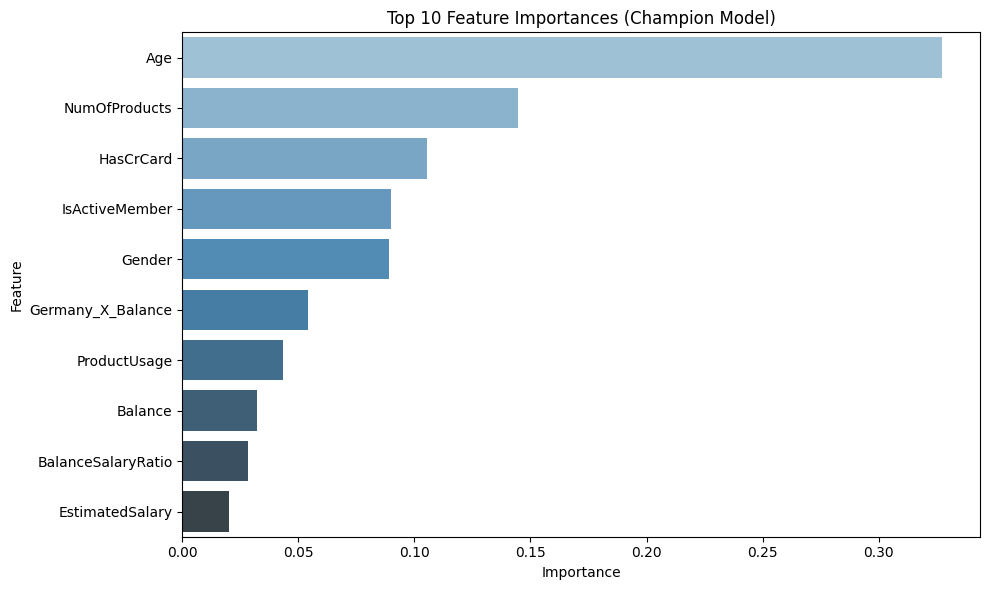

Technique: Feature Selection

Top Predictive Drivers

Age and number of products emerged as the strongest signals for model convergence.

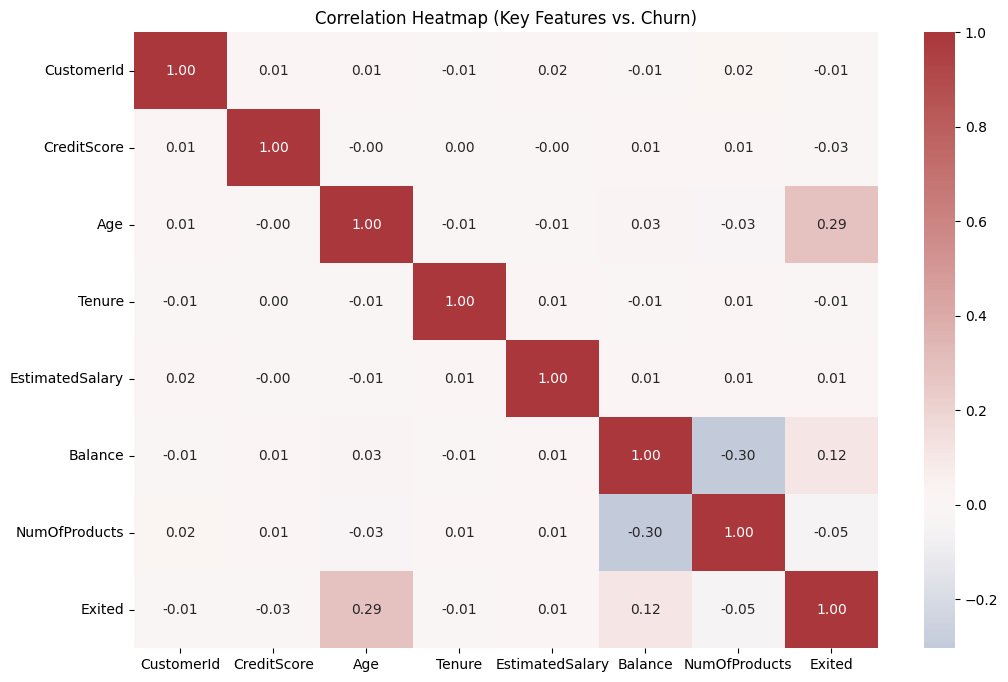

Technique: EDA

Multivariable Correlation

Heatmap identified redundant features and validated hypothesize interaction terms.

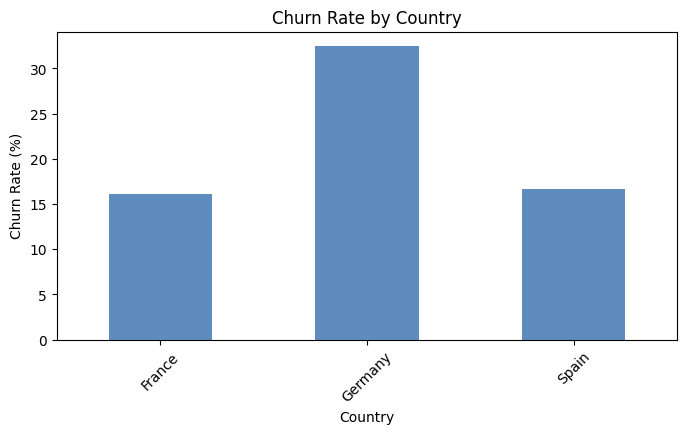

Technique: Spatial Analysis

Geographic Leakage

German customers exhibited a unique churn profile tied specifically to account balance.

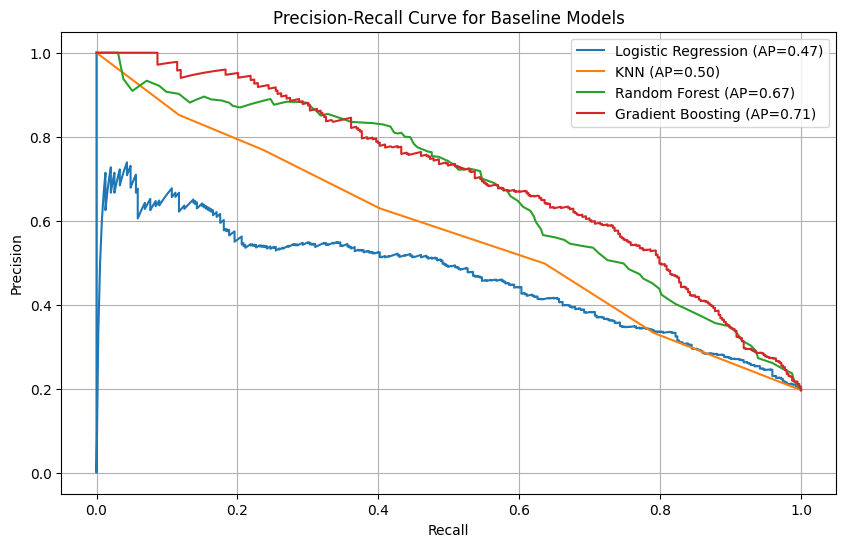

Technique: Performance Tuning

Precision-Recall Curve

Decision threshold tuned specifically to 0.45 to maximize recall for high-risk accounts.

The Analytical Workflow

Data Preparation & Cleaning

Handled extreme class imbalance using SMOTE. Engineered interaction features like `BalanceSalaryRatio` and `Germany_X_Balance` to capture subtle risk profiles missed by baseline models.

Hyperparameter Optimization

Utilized `GridSearchCV` and `RandomizedSearchCV` to optimize the Gradient Boosting champion. Balanced complexity vs accuracy to avoid overfitting to the training set.

Strategic Threshold Tuning

Calibrated the model to a 0.45 threshold. This maximized churner identification (74% Recall) while maintaining a precision actionable for business retention interventions.

Strategic Roadmap

- • Offer pre-approved credit cards to low-product accounts to deepen integration.

- • Trigger automated "Activity Nudges" for members flagging as inactive.

Geographic Focus

- • Specialized German retention desk focused on high-balance deposit rate matching.

- • Targeted financial advice campaigns for aged customer segments.

Technical Stack

Analyst Summary

"Predictive churn modeling isn't just about accuracy; it's about identifying the levers that can actually be pulled. By isolating inaction and product depth, we provide the bank with a direct operational script."

Github Repository